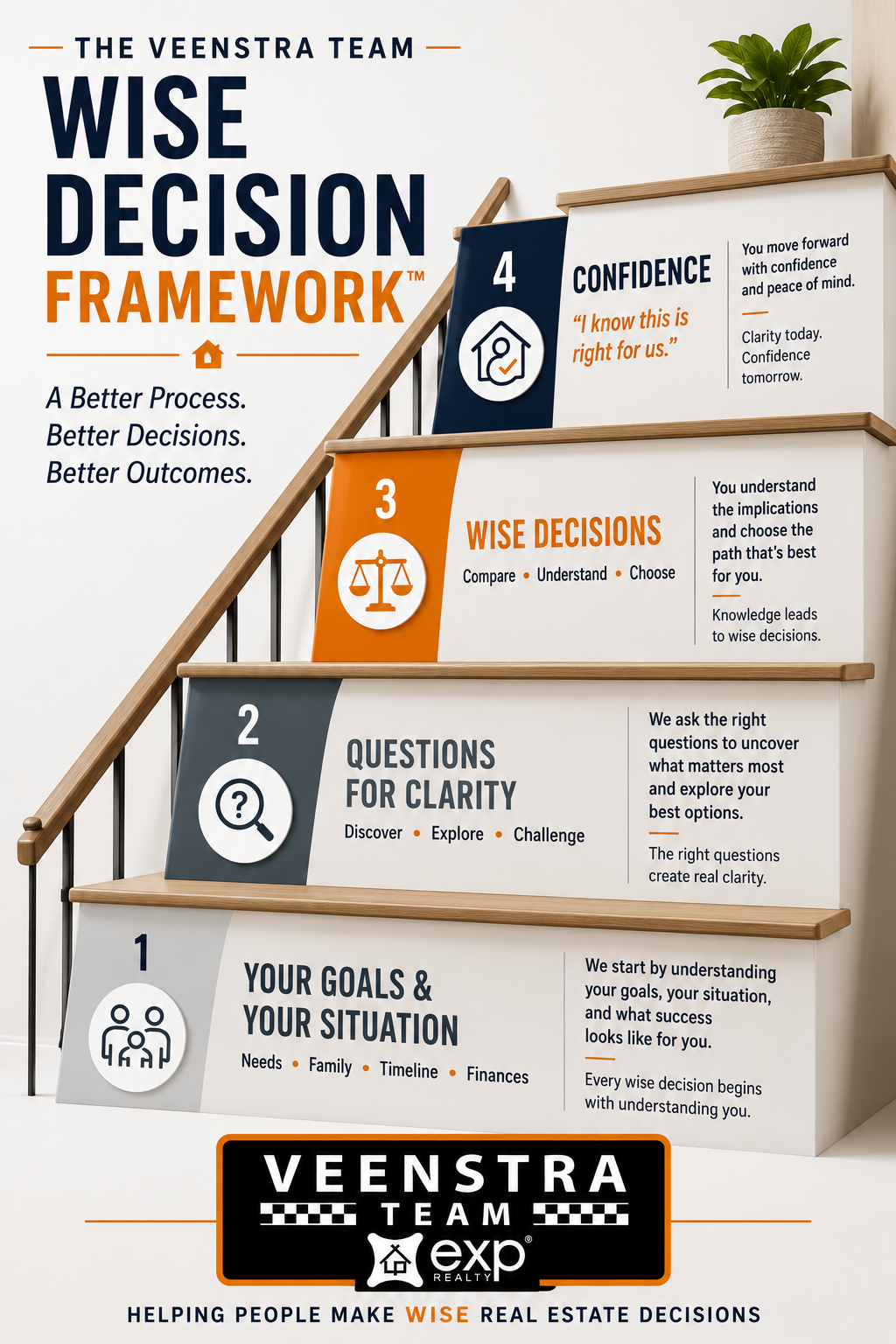

A Home Seller's Guide to Making a Wise Decision

By the Veenstra Team | Helping People Make Wise Real Estate Decisions

There Are More Ways to Sell a Home Than Most People Realize

One of the things we've learned after helping hundreds of families buy and sell homes is that no two transactions are exactly alike.

Most sales are fairly straightforward. A buyer applies for a mortgage, the bank approves the loan, everyone meets at the closing table, and the seller receives a check.

Occasionally, however, a conversation takes a different direction.

A buyer asks, "Would you consider seller financing?"

For many homeowners, that's not a question they were expecting. In fact, most have never considered the possibility of becoming the lender instead of receiving all of their money at closing.

Our experience has been that sellers usually respond one of two ways. Some immediately say, "Absolutely not." Others immediately say, "Sure, if it helps make the sale."

Neither response is necessarily the right one.

Before deciding, it's worth taking a step back and asking a different question. **What problem are we really trying to solve? **Sometimes seller financing is the perfect solution. Sometimes it creates unnecessary risk.

Most often, the answer depends on understanding your financial goals, your tolerance for risk, and whether there might be a better way to structure the transaction.

That's the purpose of this guide.

Rather than telling you what you should do, we want to help you understand the opportunities, the risks, and the questions worth asking before making one of the largest financial decisions of your life.

What Does Seller Financing Actually Mean?

At its simplest, seller financing means the buyer borrows money from you instead of borrowing it from a bank.

You and the buyer agree on the purchase price, the down payment, the interest rate, the monthly payment, and how long the financing will last. Those terms are documented in legal agreements prepared by an attorney, and the buyer begins making payments directly to you after closing.

That sounds fairly simple.

In reality, there is much more to consider.

When a bank makes a loan, they don't simply hand someone the money and hope everything works out. They carefully review income, assets, employment history, credit reports, property value, insurance, and dozens of other details before deciding whether the loan makes sense. If you become the lender, many of those same questions become your questions. That doesn't mean seller financing is a bad idea.

It simply means you're making an investment decision—not just a real estate decision.

Why Would a Seller Even Consider It?

At first glance, seller financing sounds like more work.

So why do some sellers intentionally choose it?

The answer is that it can accomplish goals that a traditional sale sometimes can't.

Perhaps you're approaching retirement and would actually prefer receiving monthly income instead of investing a large lump sum all at once.

Maybe you're selling a unique property that banks don't particularly like to finance. Around Southwest Michigan, we occasionally see this with recreational land, waterfront cottages, acreage, farms, mixed-use properties, or homes that simply don't have good comparable sales.

Sometimes the challenge isn't the property at all.

The buyer may have excellent income, strong assets, and every intention of paying their obligations, but they happen to be self-employed, relocating, waiting for another property to sell, or dealing with another temporary financing hurdle.

Seller financing can sometimes bridge those gaps.

It may also attract buyers who otherwise wouldn't consider your property because financing appeared difficult.

For some sellers, it becomes another negotiating tool. A buyer who appreciates flexible financing may be willing to agree to stronger terms, a larger down payment, or a purchase price that better reflects the property's value.

That doesn't mean seller financing is always the better choice.

It simply means there are legitimate reasons to consider it before automatically saying no.

Becoming the Bank Changes the Conversation

This is probably the most important concept in this entire guide.

When you offer seller financing, you're no longer asking only one question:

**"Do I want to sell my house?" **You're asking a second question as well:

**"Do I want to loan someone a significant amount of money?" **Those are two very different decisions.

Banks make loans every day because they've developed systems that help protect their investment.

They require down payments because buyers who have invested their own money are generally less likely to walk away.

They verify income because good intentions don't make monthly payments.

They require insurance because unexpected things happen.

They monitor taxes because unpaid taxes can create serious legal issues.

They're not trying to make the process difficult.

They're protecting an investment.

If you decide to offer seller financing, you'll want to think through many of those same issues—not because you distrust the buyer, but because you're making a financial investment that deserves careful consideration.

Fortunately, becoming the bank doesn't have to mean carrying the entire purchase price for thirty years.

In fact, that's one of the biggest misconceptions about seller financing.

Seller Financing Isn't Just One Thing

One of the questions we hear fairly often is:

"If I agree to seller financing, does that mean I'm financing the entire house?"

Not at all. In fact, one of the biggest surprises for many homeowners is discovering just how flexible seller financing can be.

Sometimes the seller finances the entire purchase price.

Sometimes they finance only a small portion.

Sometimes financing lasts only a few months.

Sometimes it's designed to create retirement income for many years.

Sometimes it's simply a way to help a buyer bridge the gap until another home sells.

The structure should fit the situation.

That's why understanding the different types of seller financing is so important. Rather than thinking of seller financing as a single option, it's more helpful to think of it as a toolbox. Each tool solves a different problem. The question isn't, **"Which one is best?" **The better question is, "Which one best fits my goals while appropriately protecting my investment?"

The following sections explain the most common approaches, along with situations where each may—or may not—be a good fit.

Seller financing can play out in many ways.

Understanding the Different Types of Seller Financing

One of the biggest misconceptions about seller financing is that it's a single financing method. It isn't.

Think of seller financing as a toolbox rather than a single tool. Each financing structure was developed to solve a different problem. Some are designed to create long-term retirement income. Others simply help a buyer overcome a temporary obstacle. Some provide more protection for the seller, while others provide greater flexibility for the buyer.

Our role isn't to tell you which one is best. It's to help you understand what each one accomplishes so you can decide whether it aligns with your financial goals and comfort level.

Let's look at the most common approaches.

Seller Mortgage (The Seller Becomes the Bank)

When most people think of seller financing, this is usually what comes to mind.

The buyer purchases the home, receives the deed at closing, and signs a promissory note and mortgage agreeing to repay the seller over time. Instead of mailing a payment to a bank each month, the buyer sends it to you or to a professional loan servicing company acting on your behalf.

For many sellers, this arrangement feels very familiar because it closely resembles a traditional mortgage.

Why sellers sometimes choose this approach

Ownership transfers immediately.

The seller earns interest on the money being financed.

Monthly payments can provide predictable retirement income.

Buyers often appreciate the flexibility compared to conventional lending.

Things to think about

While ownership transfers immediately, your financial interest in the property remains until the loan is repaid. If the buyer stops making payments, you may have to pursue foreclosure just as a bank would.

For that reason, we generally encourage sellers to think carefully about the buyer's financial strength before agreeing to this type of financing.

The Michigan Favorite: Land Contracts

If you've lived in Michigan very long, you've probably heard someone say they "bought the property on land contract."

Land contracts have been used successfully throughout Michigan for generations and remain one of the more common forms of seller financing.

Unlike a traditional mortgage, the buyer usually takes possession of the property immediately, but the seller keeps legal title until the terms of the contract have been satisfied. Once the buyer fulfills those obligations, the deed is transferred.

Many sellers appreciate this approach because retaining legal title provides an additional level of security during the repayment period.

Why some sellers prefer land contracts

The seller retains legal title until the agreement is completed.

Land contracts have a long history of use in Michigan.

Buyers who cannot obtain conventional financing may still have an opportunity to purchase.

The terms can often be customized to fit both parties.

Important things to think about: Land contracts are not simply "handshake agreements."

They should be professionally prepared, properly recorded when appropriate, and reviewed by an attorney familiar with Michigan real estate law. Default procedures differ from traditional mortgages, so understanding those differences before signing is important.

Balloon Financing

Sometimes both the buyer and seller know from the beginning that they don't want a financing relationship lasting thirty years.

Instead, they agree that the buyer will make monthly payments for a shorter period—perhaps three, five, or seven years. At the end of that period, the remaining balance becomes due in one payment, commonly called a balloon payment.

The expectation is usually that the buyer will refinance with a traditional lender before the balloon comes due.

Why sellers like balloon financing

It limits long-term risk.

The seller receives monthly income for several years.

The seller receives the remaining balance sooner.

Buyers have time to strengthen their financial position before refinancing.

Things to think about

The biggest question isn't whether the payments will be made during the first few years. It's whether the buyer will realistically be able to refinance when the balloon payment becomes due. That conversation should happen before the agreement is signed—not five years later.

Interest-Only Financing

Occasionally, buyers need lower monthly payments for a temporary period.

Rather than paying both principal and interest each month, they pay only the interest for an agreed period of time. The principal is repaid later, often through refinancing or a balloon payment.

This structure is most commonly used when the buyer expects a significant financial event in the near future, such as the sale of another property, completion of construction, or increased business income.

Why sellers sometimes consider it

Monthly payments are lower for the buyer.

The seller continues earning interest.

It can help otherwise qualified buyers complete a purchase.

Things to think about

Because the loan balance doesn't decrease during the interest-only period, the seller's exposure remains largely unchanged. This type of financing generally works best when everyone has a clear plan for how and when the principal will eventually be repaid.

Wraparound Financing

Wraparound financing is one of the least understood forms of seller financing.

It occurs when the seller still has an existing mortgage on the property but creates a new loan for the buyer that "wraps around" the original loan. The buyer makes payments to the seller, and the seller continues making payments to the original lender.

There are situations where this can be an effective financing tool.

There are also situations where it can create significant legal and financial complications.

Why it may be considered

An existing mortgage may have an attractive interest rate.

It can create financing opportunities that otherwise wouldn't exist.

Things to think about

Many mortgages contain what is known as a "due-on-sale" clause, giving the lender the right to require the loan to be paid in full if ownership changes. Because of those potential complications, wraparound financing should never be entered into without experienced legal advice.

Lease with an Option to Purchase

Although this isn't technically seller financing at the beginning, it's frequently discussed alongside seller financing because it can create a pathway toward homeownership.

The buyer leases the property for a period of time while receiving the option to purchase it later. Sometimes a portion of the rent or an upfront option fee is credited toward the future purchase price.

This arrangement gives buyers time to improve their credit, accumulate additional savings, or resolve temporary financing challenges.

Why sellers consider this option

It generates rental income.

It provides buyers additional time to qualify for financing.

It creates another avenue for selling a property that might otherwise sit on the market.

Things to think about

During the lease period, you remain the property owner—not just the lender. That means you're also assuming many of the responsibilities that come with being a landlord.

Which Type Is Best?

One of the questions we're asked most often is,

"Which one do you recommend?" Our answer is almost always the same. It depends on what you're trying to accomplish.

If your goal is to create retirement income, one approach may make sense.

If your goal is simply helping a buyer bridge the gap until another home sells, an entirely different structure may be appropriate.

If your goal is limiting risk as much as possible, your financing terms will probably look very different than someone whose primary objective is maximizing monthly cash flow.

That's why we rarely begin the conversation by talking about documents or financing structures.

Instead, we begin by asking questions.

What are your financial goals?

How quickly do you need your money?

How comfortable are you accepting risk?

Would you be comfortable owning the property again if circumstances changed?

Once those answers become clear, the appropriate financing structure often becomes much clearer as well.

Fortunately, there are even more ways to customize seller financing than the traditional methods we've discussed so far. In the next section, we'll explore some of the creative financing strategies that can solve very specific problems without requiring the seller to finance the entire purchase price.

Creative Seller Financing Strategies

One of our favorite parts of helping people through a real estate transaction is finding solutions that allow everyone to accomplish their goals. Sometimes that means negotiating a better price. Sometimes it's changing the closing date. Sometimes it's finding a lender with a different loan program. And occasionally, it means structuring seller financing in a way that solves a very specific problem without asking the seller to finance the entire purchase.

This is where seller financing becomes much more interesting. Most people assume the seller either finances the whole transaction or doesn't finance it at all. In reality, many successful transactions involve the seller financing only a small piece of the puzzle. Let's look at some of the more common examples.

Carrying a Second Mortgage

This is probably the most practical form of seller financing, yet many homeowners don't realize it's even possible.

Instead of financing the entire purchase price, the buyer obtains a traditional mortgage from a bank for most of the purchase price, and the seller finances only the remaining balance. Imagine your home sells for $500,000. The buyer obtains a mortgage for $425,000 and brings $25,000 as a down payment. Rather than reducing your price because the buyer is short $50,000, you agree to finance that portion yourself. Instead of carrying a half-million-dollar loan, you're financing only ten percent of the purchase price.

Many sellers appreciate this approach because it limits their exposure while still making the transaction possible.

Why sellers like this strategy

You're financing a much smaller amount.

The buyer has already qualified with a conventional lender.

You earn interest on the amount you're financing.

The buyer has significant motivation to protect both loans.

Important consideration

Because the bank holds the first mortgage, its loan generally has priority if the property were ever foreclosed upon. That doesn't automatically make this a poor choice, but it's something sellers should fully understand before agreeing to the arrangement.

Bridging the Gap Until Another Home Sells

We see this situation fairly often. A buyer has plenty of equity.The problem is that it's tied up in their current home. They can comfortably afford your property, but they can't access their equity until their existing home sells. Rather than losing the sale, some sellers agree to finance a portion of the purchase for a relatively short period of time. Once the buyer's home sells, your loan is paid off. Instead of becoming a long-term lender, you've simply helped bridge a temporary timing issue. For many sellers, that's a much more comfortable conversation.

Solving an Appraisal Gap

This is one of the least talked about uses of seller financing. Suppose you agree to sell your home for $500,000. Everything is moving forward until the appraisal comes back at $480,000.

Now everyone has a problem. The bank will lend based upon the appraised value—not the purchase price. At this point, several things could happen. The buyer might bring another $20,000 to closing. You might reduce your price.

Or...

You might finance the difference. Instead of losing the sale or reducing your price, you create a second mortgage for the amount the bank won't finance. The buyer purchases the home at the agreed price, and you receive interest on the remaining balance. Not every appraisal gap should be handled this way, but it's one more example of how seller financing can solve a very specific problem.

Land Financing

Vacant land often presents financing challenges. Many lenders require larger down payments for land purchases, and some simply aren't interested in making smaller land loans. If your buyer plans to build, seller financing may only be needed for the land itself. The buyer purchases the property, begins construction using a construction loan, and later refinances everything into one permanent mortgage.

Rather than financing a completed home for decades, you've simply helped move the project forward.

Helping a Buyer Who Is Self-Employed

Self-employed buyers sometimes find themselves in an interesting position. They may have substantial income and excellent cash flow, yet conventional lenders require additional years of tax returns or business history before approving a mortgage. That doesn't necessarily make them a risky borrower. It simply means their financial story doesn't fit neatly into a lender's underwriting guidelines. Sometimes seller financing provides enough time for the buyer to meet those requirements. A balloon payment due in three or five years may give the buyer time to refinance conventionally while allowing the seller to receive full payment within a reasonable period.

Family Transactions

Some of the most rewarding transactions we've been involved with have taken place within families. Parents helping children. Grandparents helping grandchildren. Family cottages passing to the next generation.

Seller financing can make those transitions easier while allowing the seller to receive income over time instead of requiring family members to obtain outside financing. We've also found that these transactions deserve every bit as much documentation as transactions between strangers. Good legal documents protect relationships. When expectations are clearly defined from the beginning, misunderstandings become much less likely later.

Seasonal Income Doesn't Always Fit Monthly Payments

Not everyone receives the same paycheck every two weeks. Business owners, farmers, commission sales professionals and seasonal workers often experience periods of high income followed by slower months. Traditional mortgages generally don't accommodate those realities. Seller financing sometimes can.

Instead of twelve identical payments, the parties may agree to quarterly payments, seasonal adjustments, or one larger payment after a business's busy season. Again, the goal isn't simply to make financing easier. The goal is to create a payment schedule that realistically matches the buyer's ability to pay while still protecting the seller's investment.

Sometimes the Best Solution Isn't Seller Financing at All

One of the reasons we enjoy these conversations is because they often uncover better solutions.

A buyer may think they need seller financing when a portfolio lender would gladly make the loan.

A seller may assume they have to finance the entire purchase price when financing only a small portion would accomplish the same goal.

Sometimes extending the closing date by sixty days solves the problem.

Sometimes a bridge loan is available.

Sometimes another lending program makes everything unnecessary.

That's why we believe seller financing should almost never be the starting point.

It should be one of several tools considered after everyone understands the situation.

A Good Financing Plan Solves a Problem

As we've worked through these different financing strategies, you may have noticed a common theme.

The best seller financing arrangements aren't built around documents.

They're built around problems.

Every successful financing structure begins with understanding what obstacle is standing in the way of a successful closing.

Once that obstacle is identified, there is often more than one solution.

Sometimes seller financing is one of them. Sometimes it isn't.

The next step is deciding whether you're personally comfortable becoming the lender.

That decision has less to do with financing structures and much more to do with your financial goals, your tolerance for risk, and the questions every seller should honestly ask before making that commitment.

Twenty-Five Questions Every Seller Should Ask Before Offering Seller Financing

By now, you've probably realized that seller financing isn't simply a financing decision. It's also an investment decision. One of the reasons banks spend so much time evaluating borrowers is because they know something most of us learn only through experience:

The quality of the loan is usually determined before the first payment is ever made.

The questions asked before closing often become the difference between a successful investment and a stressful one. Over the years, we've found that the best seller financing decisions begin with honest conversations. Not just conversations with the buyer, but conversations with yourself. The following questions aren't intended to discourage seller financing. They're intended to help you understand the risk and to help you think through the decision from every angle before committing to it.

Part One: Does Seller Financing Fit My Financial Goals?

Before evaluating the buyer, it's worth evaluating your own situation. Many sellers immediately begin asking whether the buyer is trustworthy. We think the better place to start is with yourself.

If seller financing doesn't fit your financial goals, it probably doesn't matter how qualified the buyer is.

Ask yourself:

Do I actually need all of my money at closing?

Would monthly income fit my retirement plans better than one lump sum?

Am I depending on these proceeds to purchase another home?

Would tying up some of my equity limit future opportunities?

If interest rates change, would I still feel good about this decision five years from now?

If your answer to several of these questions is "I'm not sure," that's perfectly normal. It simply means this deserves a deeper conversation before moving forward.

Part Two: How Much Risk Am I Comfortable Accepting?

Every investment involves some level of risk. Seller financing is no different.

The question isn't whether risk exists. The question is whether you're comfortable with the amount of risk you're accepting in exchange for the potential benefits.

Consider these questions:

Would I lose sleep worrying about this loan?

Could I financially handle a period of missed payments?

If property values declined, would I still feel adequately protected?

Am I comfortable making decisions that a bank would normally make?

If I had to enforce the terms of the agreement, would I actually be willing to do it?

One of the hardest realities of seller financing is that good people sometimes experience financial hardship. Preparing for that possibility doesn't mean you expect it to happen. It simply means you're making decisions with both your head and your heart.

Part Three: Am I Comfortable Owning This Property Again?

This question catches many sellers by surprise. We almost always ask it anyway.

"If you had to take this property back three years from now, would you still want to own it?"

If your immediate response is, "Absolutely not," that's worth paying attention to. No one enters seller financing expecting foreclosure. But every lender has to consider that possibility. If circumstances changed, would the property still fit your financial goals? Would you be comfortable managing it? Would it still be desirable? Would it still be marketable?

Sometimes the answer is yes. Sometimes the answer quickly helps sellers realize they would rather receive full payment at closing and move on.

Part Four: Is the Buyer Financially Ready?

It's natural to like the buyer. It's also important to evaluate the buyer. Those are two different things.

Banks don't approve loans because people seem trustworthy.

They approve loans because the financial information supports the decision.

The same principle applies here.

Questions worth asking include:

Why isn't conventional financing being used?

Is the situation temporary or long-term?

Has the buyer demonstrated the ability to make the payments?

Is the requested financing solving a legitimate problem?

Has income been verified?

Are sufficient financial records available?

Does the buyer have meaningful cash invested in the purchase?

The answers to these questions often matter much more than a credit score by itself.

Part Five: How Should the Loan Be Structured?

One of the biggest advantages of seller financing is flexibility. Unlike a traditional mortgage, nearly every term is negotiable. That flexibility is valuable.

It also means careful thought should go into the structure before documents are prepared.

Questions to consider

How much of a down payment would make me comfortable?

Should the loan last three years, five years, or longer?

Would I prefer a balloon payment?

What interest rate fairly compensates me for the risk?

Should taxes and insurance be escrowed?

Who will collect the monthly payments?

Should a professional loan servicing company be involved?

There isn't one correct answer. The best structure is the one that appropriately balances opportunity with protection.

Part Six: Have I Built the Right Professional Team?

One of the easiest mistakes sellers make is assuming seller financing is simply another purchase agreement. It isn't. You're creating a loan. That means your team matters.

An experienced real estate professional, attorney, title company, CPA and, in many cases, a loan servicing company all play important roles. Trying to save a little money by skipping professional advice often becomes far more expensive later.

Part Seven: What Happens If Life Doesn't Go According to Plan?

This isn't a pleasant conversation. It's also one of the most important. Life changes. People lose jobs. Health changes. Businesses struggle. People pass away. Good planning isn't about expecting the worst. It's about making sure everyone understands what happens if circumstances change.

Questions worth discussing

What happens if the buyer misses payments?

What happens if the property is damaged?

What happens if either party dies before the loan is paid?

Can the note be sold if additional cash is needed?

How will disputes be resolved?

Thinking through these possibilities now is far easier than trying to solve them during a crisis.

A Simple Checklist Before You Say "Yes"

Sometimes the best way to summarize a big decision is with a simple checklist. Before agreeing to seller financing, ask yourself whether each of these statements is true.

I understand how the proposed financing works.

I don't need all of my proceeds immediately.

I'm comfortable with the level of risk involved.

I would be comfortable owning this property again if circumstances required it.

I understand why the buyer is requesting seller financing.

The buyer has demonstrated the ability to repay the loan.

I'm satisfied with the proposed down payment.

The interest rate appropriately reflects the risk I'm accepting.

My attorney and CPA have reviewed the transaction.

I'm making this decision because it supports my financial goals—not because I feel pressured to do so.

If you can confidently answer "yes" to each of those statements, you're in a much stronger position to decide whether seller financing is the right fit for your situation.

In the next section, we'll look at some of the most common mistakes sellers make when offering seller financing—and how a little planning can prevent many of them.

Common Mistakes Sellers Make When Offering Seller Financing

One of the reasons we wanted to write this guide is because we've seen sellers make decisions based on assumptions instead of information. Most of these mistakes aren't made because someone was careless. They're made because the seller was trying to help, wanted to keep a transaction together, or simply didn't realize there was a better way to structure the agreement.

Fortunately, nearly all of these mistakes can be avoided with good planning and the right team of professionals.

Mistake #1: Falling in Love with the Buyer's Story

One of the easiest things to do is become emotionally invested in the buyer. Perhaps they're a young family trying to purchase their first home. Maybe they're relocating to care for aging parents. Perhaps they're self-employed and frustrated because a bank doesn't understand their financial situation.

**Those stories matter. But stories should never replace financial due diligence. **Banks don't make lending decisions based on how much they like someone. They make lending decisions based on whether the borrower has demonstrated the ability to repay the loan.

**The same principle applies here. **It's perfectly appropriate to appreciate the buyer's circumstances while still asking for financial documentation.

Those two things are not in conflict.

Mistake #2: Accepting Too Small of a Down Payment

One of the strongest indicators of a buyer's commitment is the amount of their own money invested in the purchase. A meaningful down payment demonstrates confidence, reduces the amount being financed, and gives the buyer additional incentive to protect their investment. Every transaction is different, so there isn't one percentage that's right for every situation.

The better question is this: "How much money would I want the buyer to have invested before I'd feel comfortable making this loan?"

That answer may differ from one seller to another, but it's an important conversation to have before terms are negotiated.

Mistake #3: Assuming Seller Financing Is the Only Solution

We've touched on this earlier in the guide, but it's worth repeating.Sometimes seller financing is exactly the right answer. Sometimes it isn't.

Before agreeing to finance a buyer, ask whether another solution might accomplish the same goal. The Veenstra Team has a few hand selected lenders that we often recommend. One of those lenders is so familiar with loan programs and requirements of different loans that talking to him is always our first bit of advice before we go any further down the seller financing path.

Another lender has a unique program that is able to provide "private financing" to help bridge certain circumstances.

A few of our lender partners have solid "bridge loan" options that help someone purchase a home before their current house is sold.

Perhaps a portfolio lender would approve the loan.

Perhaps extending the closing date would solve the timing issue.

Perhaps financing only a small portion of the purchase price would accomplish what everyone is trying to achieve.

The best transactions usually begin by exploring all of the available options rather than assuming seller financing is the only path forward and this is why is is so important to work with a REALTOR that understands the bigger picture, that has a large tool bag of options to suggest and that has a proven track record of success in helping people make wise real estate decisions. In real estate, no situation is the same. What seems like a standard, common situation has twists and turns that may surface. When the Veenstra Team works with clients, our first step is to understand your goals. Then we must understand and clarify your situation and only then can we begin to guide you to possible solutions.

Mistake #4: Trying to Save Money on Professional Advice

When seller financing comes up, it's tempting to think, *"We'll just use a standard form and keep things simple." *Unfortunately, that's rarely a good idea. Unlike a traditional purchase agreement, seller financing creates a lending relationship that may last for years.

The documents should clearly explain the responsibilities of both parties, payment terms, default provisions, insurance requirements, taxes, balloon payments if applicable, and many other important details. Having an attorney prepare or review those documents is usually one of the least expensive parts of the transaction—and one of the most valuable.

Mistake #5: Collecting Payments Yourself

Some sellers enjoy receiving the monthly payments directly. Others quickly discover that collecting payments, tracking balances, calculating interest, monitoring insurance, and maintaining accurate records isn't something they want to do for the next several years.

Professional loan servicing companies exist for a reason.For a relatively modest fee, they can collect payments, maintain records, provide annual statements, monitor escrow accounts when applicable, and help remove some of the awkwardness that can develop if a payment is late. For many sellers, it's money well spent.

Mistake #6: Not Thinking About Taxes

Most sellers immediately focus on the interest they'll receive. Far fewer think about the tax implications.

Seller financing may affect:

Capital gains reporting

Interest income

Depreciation recapture on investment property

Estate planning

Future tax liability

None of these are reasons to avoid seller financing.

They're simply reminders that your CPA should be part of the conversation before the documents are signed—not after.

Mistake #7: Forgetting About Insurance and Property Taxes

One question we often hear is, *"If I finance the sale, who makes sure the taxes and insurance are paid?" *That's an excellent question. One of the reasons lenders require proof of insurance and often collect escrow payments is because the property serves as collateral for the loan. If taxes become delinquent or insurance lapses, the seller's investment may be exposed to unnecessary risk.

Your attorney and loan servicing company can help structure an agreement that addresses these issues appropriately.

Mistake #8: Assuming Everyone Will Remember What Was Agreed To

It's amazing how quickly people can remember a conversation differently. That's why we encourage putting important expectations in writing. Good documentation protects everyone involved. It reduces misunderstandings. It provides clarity.

Most importantly, it allows both buyer and seller to move forward with confidence, knowing everyone is working from the same understanding.

Mistake #9: Not Having a Plan if Things Go Wrong

No one expects the buyer to stop making payments. No one expects unexpected illness. No one expects a business failure. But lenders prepare for those possibilities anyway. One of the healthiest conversations a seller can have is this:

"If life doesn't go according to plan, what happens next?"

Discussing those possibilities before closing isn't pessimistic. It's simply part of responsible planning.

Mistake #10: Making the Decision Too Quickly

This may be the most common mistake of all. Seller financing is often introduced late in negotiations. The buyer is excited. The seller wants to keep the transaction together. Everyone wants to reach the closing table. That's exactly when it's important to slow down. Take time to understand the proposal. Review the numbers. Ask questions. Talk with your attorney. Talk with your CPA.

There is rarely a disadvantage to making a thoughtful decision. There can be significant consequences from making a rushed one.

The Veenstra Team Perspective

One of the things we appreciate most about seller financing is that it encourages thoughtful conversations. Sometimes those conversations lead to a seller-financed transaction. More often they lead to a conventional mortgage. Sometimes they uncover an entirely different solution that neither party had considered.

We consider all three outcomes to be successful. Our job isn't to convince you to offer seller financing or to tell you it is never a good option. Our job is to help you understand the implications of every option available so you can choose the one that best supports your goals.

In the next section, we'll pull everything together by discussing who is generally a good candidate for seller financing, who may be better served by a traditional sale, and how to decide which path is right for you.

Is Seller Financing Right for You?

After everything we've covered, you may still be wondering: "So...should I offer seller financing?"

The honest answer is the same one we give our clients. It depends.

Not because we're trying to avoid the question, but because seller financing isn't simply a financial tool. It has to fit your goals, your stage of life, your tolerance for risk, and the unique circumstances surrounding your property and your buyer. Some sellers are excellent candidates for seller financing. Others are much better served by receiving all of their proceeds at closing and moving on.

The important thing isn't choosing the "right" answer. The important thing is choosing the right answer for you.

Seller Financing May Be Worth Exploring If...

Over the years, we've noticed several situations where seller financing often deserves a closer look.

You don't need all of your proceeds immediately.

Perhaps you've paid off your mortgage years ago, you're financially secure, and receiving monthly income would actually be more valuable than receiving one large check.

For many retirees, predictable monthly cash flow can become an attractive part of an overall financial plan.

You're selling a unique property.

Some properties don't fit neatly into conventional lending guidelines. Lake cottages. Large acreage. Vacant land. Family farms. Mixed-use properties. Properties with limited comparable sales.

These types of properties sometimes require creative thinking, and seller financing may open doors for buyers who otherwise couldn't purchase them.

The buyer has a temporary obstacle—not a permanent one.

This is an important distinction. There's a significant difference between someone who can't qualify for financing and someone who doesn't yet qualify because of timing.

Perhaps they're relocating. Perhaps they're self-employed and need another year of tax returns. Perhaps they're waiting for another property to sell. Perhaps an appraisal issue needs to be solved. Temporary challenges sometimes justify temporary financing solutions.

You're comfortable thinking like an investor.

One of the best seller-financed transactions is one where the seller truly understands they're making an investment. They're comfortable evaluating risk. They're patient. They've involved their attorney and CPA. They're making a business decision rather than an emotional one.

Seller Financing May Not Be the Best Choice If...

Seller financing isn't the right answer for every seller. In fact, many homeowners are better served by a traditional sale.

You need all of your equity immediately.

If you're depending on your sale proceeds to purchase another home, pay off debt, fund retirement, or accomplish another financial goal, tying up your equity may create unnecessary stress. There's nothing wrong with wanting the simplicity of a traditional closing.

You know you would constantly worry about the loan.

Some people are simply not comfortable lending money. That's okay. If you'd find yourself wondering every month whether the payment will arrive... If you'd lose sleep over the possibility of default... If you'd constantly worry about the property... Seller financing may not be worth the emotional cost, regardless of the financial return.

You never want to own the property again.

This question continues to be one of our favorites. If circumstances required you to take the property back... Would you? If the answer is an immediate "No," that deserves serious consideration. Every lender must consider the possibility of default. There's no reason you shouldn't do the same.

The buyer hasn't demonstrated financial readiness.

Wanting the property isn't enough. Neither is having a compelling story. Seller financing should be based upon evidence that the buyer has both the ability and the commitment to meet their obligations. Helping someone purchase a home is generous. Ignoring warning signs rarely helps either party.

There Isn't Always a Right Answer

One thing we've learned over the years is that good real estate decisions rarely come from rigid rules. Two sellers with nearly identical homes may make completely different decisions—and both may be right. One seller may value immediate liquidity. Another may value long-term income. One seller may enjoy making investments. Another may prefer eliminating uncertainty. Neither approach is better. They're simply different. That's why we encourage our clients to avoid making decisions based solely on what someone else did. Instead, make the decision that best supports your financial goals, your family, and your future.

How We Help Our Clients Evaluate Seller Financing

When seller financing becomes part of the conversation, our first instinct isn't to start filling in blanks on a contract. It's to start asking questions.

What is the buyer trying to accomplish?

What is the seller trying to accomplish?

Is seller financing truly the best solution, or is there another option that better serves everyone involved?

If seller financing appears to make sense, we help our clients understand the available structures, discuss the potential implications, coordinate conversations with lenders, attorneys, title companies, and CPAs, and work toward an agreement that protects everyone's interests.

Just as importantly, if we believe a traditional sale is the better path, we'll say that too. Our responsibility isn't to make every transaction work. Our responsibility is to help our clients make wise decisions—even if that means advising against seller financing.

Final Thoughts

Seller financing has helped thousands of buyers become homeowners and thousands of sellers accomplish financial goals that might not have been possible through traditional financing alone. It has also created challenges for people who entered into agreements without fully understanding the responsibilities involved.

Knowledge makes the difference. If you've read this guide from beginning to end, you're already far ahead of most homeowners considering seller financing.

You understand that seller financing isn't one financing program. It's a collection of tools.

Some are designed to create retirement income.

Some solve temporary financing challenges.

Some help unique properties find the right buyer.

Others simply aren't appropriate for a particular situation.

The goal isn't to become an expert lender overnight.

The goal is to ask thoughtful questions, assemble the right professional team, and choose the path that best supports your long-term goals.

Whether you ultimately decide to offer seller financing or accept a conventional offer, we hope this guide has given you the confidence to move forward with greater clarity. That's why we created it. Because helping people make wise real estate decisions has always been at the heart of what we do.

What's Next?

In the final section of this guide, we'll answer many of the most common questions homeowners ask about seller financing, including:

Is seller financing common in Michigan?

Are land contracts still legal?

How is the interest rate determined?

What happens if the buyer stops making payments?

Can the seller sell the note later?

Who pays property taxes and insurance?

What professionals should be involved?

What are the tax implications?

Can seller financing help sell a difficult property?

How does the Veenstra Team help guide these conversations?

Frequently Asked Questions About Seller Financing

As we've worked with buyers and sellers over the years, we've found that many of the same questions come up again and again. Some are practical. Some are legal. Some are financial. None of them are unimportant.

If you're considering seller financing, these are excellent questions to discuss with your REALTOR®, attorney, CPA, and lender before making a final decision.

Is Seller Financing Legal in Michigan?

Yes. Seller financing is completely legal in Michigan when it is properly structured and documented. Depending on the situation, the transaction may involve a mortgage, a land contract, a promissory note, or another legal financing arrangement. Each has its own legal requirements, so it's important to work with an attorney experienced in Michigan real estate law.

Are Land Contracts Still Used?

Absolutely. Although they are less common than they once were, land contracts continue to be used throughout Michigan, particularly for vacant land, unique properties, family transactions, and situations where conventional financing isn't the best fit. Like any financing arrangement, they should be carefully drafted and fully understood by both parties before signing.

How Much Should the Buyer Put Down?

There isn't a single answer that fits every transaction. Generally speaking, a larger down payment reduces the seller's risk because the buyer has more of their own money invested in the property. Rather than asking, "What's the minimum?" We encourage sellers to ask, **"What amount would make me feel comfortable making this loan?" **The answer may be different for every seller.

Who Decides the Interest Rate?

Unlike a conventional mortgage, there isn't a published rate sheet that determines the interest rate. The buyer and seller negotiate the terms together. The agreed-upon rate should fairly compensate the seller for the risk being assumed while remaining reasonable for the buyer. Market conditions, loan length, down payment, and overall risk all play a role in that conversation.

Who Collects the Monthly Payments?

Many sellers choose to hire a professional loan servicing company. The servicing company collects the payments, maintains payment records, prepares year-end statements, monitors escrow accounts if required, and helps ensure accurate record keeping. Some sellers collect payments themselves. Others find that professional servicing removes much of the administrative work and helps preserve the business relationship between buyer and seller.

Who Pays Property Taxes and Homeowners Insurance?

The buyer is typically responsible for both property taxes and homeowners insurance unless the financing agreement provides otherwise. Some agreements require escrow payments so taxes and insurance are paid automatically. Others require proof that taxes and insurance remain current throughout the life of the loan. This is one of the many details that should be addressed before closing.

What Happens If the Buyer Stops Making Payments?

That depends on how the financing was structured. Mortgages, land contracts, and other financing arrangements each have different legal remedies under Michigan law. The important thing to remember is that seller financing should always include clearly written default provisions so everyone understands the process before problems arise. No one enters a transaction expecting default. Planning for the possibility simply protects everyone involved.

Can Seller Financing Help Me Sell My Home Faster?

Sometimes. Offering financing may increase the number of qualified buyers interested in your property, particularly if you're selling:

Vacant land

Waterfront property

Recreational property

Farms

Unique homes

Properties that conventional lenders sometimes struggle to finance

Seller financing doesn't automatically increase value or reduce marketing time, but it may open the door to buyers who otherwise couldn't complete the purchase.

Should I Offer Seller Financing to Anyone Who Asks?

Probably not. The request itself isn't the issue. Understanding why the buyer is requesting seller financing is. Some buyers simply need flexibility because of timing. Others may have challenges that make conventional financing unlikely in the foreseeable future. Understanding the reason behind the request is often far more important than the request itself.

What Professionals Should Be Involved?

One of the biggest themes throughout this guide has been building the right team. Seller financing is rarely something that should be handled alone. Depending on the circumstances, your team may include:

Your REALTOR®

A real estate attorney

Your CPA or tax advisor

A title company

A professional loan servicing company

The buyer's lender, if applicable

Each professional brings a different area of expertise, helping protect both buyer and seller throughout the transaction.

How Can the Veenstra Team Help?

Seller financing is NOT something that is a part of most transactions. It also isn't something we dismiss simply because it's different. Our first responsibility is to understand your goals. From there, we help evaluate whether seller financing truly makes sense or whether another solution might accomplish the same objective with less complexity or less risk. When appropriate, we help coordinate conversations with lenders, attorneys, title companies, and tax professionals while guiding the negotiation process from beginning to end.

Our role isn't to convince you one way or the other. Our role is to help you understand the implications of every option available so you can make a wise real estate decision.

About the Veenstra Team

Real estate transactions are rarely just about houses. They're about families. Retirement. Finances. Dreams. Transitions. Sometimes they're exciting. Sometimes they're emotional. Almost always, they're important. That's why we believe our job is much bigger than writing contracts or putting signs in yards.

Our responsibility is to educate, ask good questions, explain implications, solve problems creatively, and help our clients make confident decisions.

Sometimes seller financing becomes part of that solution. Sometimes it doesn't. Either way, we believe our clients deserve to understand every reasonable option before deciding what comes next. If you're considering selling your home and would like to explore whether seller financing—or another strategy—might help you accomplish your goals, we'd be honored to have that conversation.

There is never pressure. Just practical advice, thoughtful questions, and experienced guidance designed to help you make a wise real estate decision.

Click This Link To Schedule a No-Pressure Consultation

Every seller's situation is different. If you'd like to discuss whether seller financing—or another strategy—fits your goals, we'd be happy to help you think through the options. Our first conversation is about understanding your goals and your situation and your needs. If we have the expertise needed to help guide you through the selling process or the buying process, we will do all that we can to represent your best interests and make the process as smooth and clear as possible so that you can make the wisest decisions for you. If we do not have the expertise or experience needed for your particular situation, we will also tell you that. We know what we know and we know what we don't know. We have a great resource team of professionals that we can recommend when we are outside of our areas of expertise so that you can move forward with confidence.

Jason Veenstra

The Veenstra Team | eXp Realty

Helping People Make Wise Real Estate Decisions

269-350-5514

sold@veenstrateam.com

www.MyKalamazooRealEstate.com

Jason Veenstra is a REALTOR® with the Veenstra Team at eXp Realty, serving Southwest Michigan. Through the Questions Worth Asking™ series, Jason helps buyers, sellers, and builders understand the implications of important housing decisions so they can move forward with clarity and confidence. Whether you're considering seller financing, building a new home, or preparing to sell, the Veenstra Team is committed to helping people make wise real estate decisions.